In any rapidly ascending economy, the expansion of credit acts as a primary combustion engine for growth. However, this engine inevitably produces a challenging byproduct: Non-Performing Loans (NPLs). For decades, the long-term health of a national financial system has been dictated not merely by its lending volume, but by its capacity for deleveraging. When "bad debt" is allowed to stagnate on a bank’s balance sheet, it chokes off liquidity and creates a systemic fragility that can paralyze a nation’s economic ambitions.

Recognizing the need for a more robust mechanism to facilitate the transfer of distressed credit risk, the National Bank of Cambodia (NBC) Prakas No. B37.026.113 (19 Feb 2026) has introduced a sophisticated regulatory framework governing "Asset Management Institutions" (AMI). This move signals a definitive transition from ad-hoc debt recovery toward a professionalized, highly regulated industry. By establishing clear rules of engagement for the acquisition, management, and resolution of distressed assets, the NBC is constructing a new financial shield designed to fortify the Kingdom’s economic stability.

This new Prakas is more than a simple compliance checklist; it is a strategic blueprint for a secondary debt market. For institutional investors and financial stakeholders, it introduces a layer of transparency and professional rigor that was previously missing.

Here are five ways this framework is fundamentally redefining how Cambodia manages the high-stakes world of asset recovery.

1. The Birth of the Specialized "Debt Surgeon"

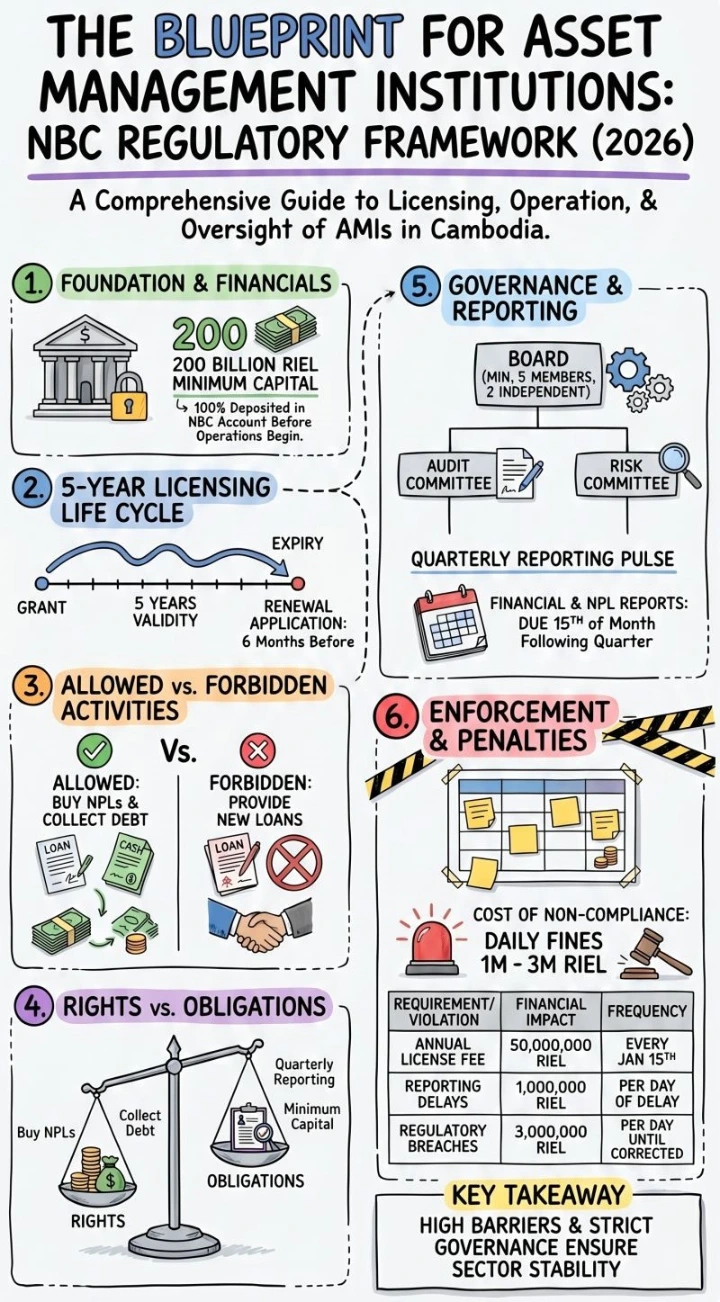

Under the new framework, the management of NPLs has transitioned from a back-office administrative burden to a specialized, licensed profession. The NBC defines an Asset Management Institution (AMI) as a licensed entity authorized to conduct "Non-Performing Loan Management." This isn't merely a collection agency; it is a specialized entity tasked with managing assets that have fallen into the technical classifications of Substandard, Doubtful, or Loss, as outlined in Article 3 of the Prakas.

This specialization allows banks to offload distressed assets to professionals who possess the focus and technical expertise required to recover value. By surgically removing these burdens from primary lenders, the regulator is encouraging a more liquid financial sector. These institutions adopt a full-lifecycle approach to debt—from strategic purchase to the legal liquidation of associated collateral.

Asset Management Institutions that have received a license from the National Bank of Cambodia may perform the following business activities:

- Purchase and manage non-performing loans and associated collateral from banks and financial institutions;

- Purchase and manage debt-related assets of banks and financial institutions through public auctions, court proceedings, or other legal processes;

- Provide debt collection services to banks and financial institutions;

- Coordinate the management of associated collateral with the consent of the debtor;

- Sell loans to other banks, financial institutions, or other Asset Management Institutions.

2. The 200 Billion Riel Regulatory Moat

The NBC is sending a clear signal: the business of asset recovery is no place for "fly-by-night" operations or undercapitalized players. To ensure that only serious, institutional-grade entities enter this space, Article 7 of the regulation establishes a formidable capital requirement. Any entity seeking an AMI license must maintain a minimum registered capital of 200,000,000,000 Riels (approximately $50 million USD).

This high barrier to entry serves as a "regulatory moat," ensuring that AMIs have sufficient "skin in the game" to manage long-term recovery processes and the complex collateral—often involving significant real estate assets—associated with them. Furthermore, the cost of operating in this regulated space includes an annual license fee of 50,000,000 Riels (approximately $12,250 USD), reinforcing the requirement for AMIs to be well-capitalized and sustainable.

3. Strict Boundaries (The "Shadow Banking" Chinese Wall)

While AMIs handle significant financial volumes, the NBC has established a strict "Chinese Wall" to prevent them from evolving into unregulated "shadow banks." Article 5 explicitly lists prohibitions that keep these institutions focused solely on credit resolution rather than credit creation. Most importantly, AMIs are strictly forbidden from:

- Providing loans or credit to the public;

- Accepting deposits from the public;

- Purchasing non-performing loans from themselves or related parties, directly or indirectly.

This last point is a critical safeguard against "circular financing." By prohibiting transactions with related parties, the regulator prevents banks from using AMIs as affiliated "garbage bins" to hide bad loans—a tactic that has historically led to major financial scandals. Their role is strictly curative: they are the cleaners of the system, not the originators of new risk.

4. Governance with "Fit and Proper" Standards

Transparency and integrity are the cornerstones of the new framework. The NBC has mandated rigorous organizational requirements, including a Board of Directors consisting of at least five members, with a minimum of two independent directors. Beyond mere numbers, Article 27 introduces "Fit and Proper" standards: board members and senior management must possess sufficient professional qualifications and have no history of criminal activity or bankruptcy.

In a forward-thinking move toward ESG (Environmental, Social, and Governance) alignment, Article 32 requires AMIs to establish a formal "Whistle Blowing Procedure." This mechanism, which remains relatively rare in Cambodian private sector regulation, is designed to protect employees who report internal irregularities or unethical behavior. In an industry as sensitive as debt recovery, this emphasis on internal integrity is vital for maintaining both public trust and investor confidence.

5. The Consumer Protection Mandate

The NBC has ensured that the human rights of the debtor are not sacrificed in the pursuit of asset recovery. The regulation aligns Cambodia with international banking standards by institutionalizing a "Resolution of Customer Complaints" procedure under Article 19.

This is not a passive requirement. Article 18 mandates that AMIs provide annual training for staff to ensure they are well-versed in professional conduct and debtor protection laws. By legally obligating AMIs to maintain professional procedures for handling grievances, the NBC prevents predatory collection practices and ensures that the transition of a loan from a bank to an asset manager does not result in a loss of legal protection for the borrower.

The Final Thought

This new framework represents a milestone in Cambodia’s financial evolution. By formalizing the role of Asset Management Institutions, the NBC is moving the country toward a sophisticated ecosystem where debt is treated as a manageable commodity rather than a systemic threat. These regulations provide the legal certainty that international investors demand and the consumer protections that the public deserves.

Will this be the catalyst that unlocks a new era of lending confidence for Cambodia's small businesses and entrepreneurs?

Disclaimer: The views expressed are solely my own and are shared for general informational and discussion purposes only. They do not constitute legal advice and should not be relied upon as a substitute for professional legal counsel. These views do not represent or reflect the positions, opinions, or policies of my current employer, any former employers, clients, or affiliated organizations. Readers are encouraged to seek advice from a qualified legal professional regarding their specific circumstances.